This post will follow up on a previous one about anti-trust. In that post, I allege that the best (if not only) way to become aggressively rich — to have “passive income” — is to abuse some “barrier to entry.” A barrier to entry is essentially some leverage that makes it very difficult for someone else to compete with you after entry.

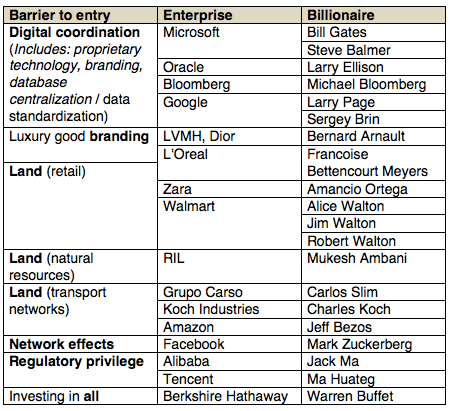

I imagine that this argument could be met with some skepticism. So I will provide an empirical argument by breaking down the wealth of the 20 richest people in the world. I am taking this list from Forbes. This is not a breakdown by industry, but an explanation of how so much wealth can be generated.

Here is my breakdown. Some of the barriers are slightly different (than the ones from the list in the other article), in order to give context.

By section:

Digital coordination

I didn’t list this one in the last article, because it’s really an umbrella term to refer to a bunch of barriers all put together. For example:

- Branding

Google and Apple especially benefit from this. People use these products and services because they know they’re familiar, easy to use, famous, and high value. More on branding later.

- Proprietary technology

It goes without saying that a “tech” firm will have proprietary technology. This might not be as big of a factor as you think, because technology can be replicated. The main thing preventing that is, of course, IP law. Google became dominant largely because they used IP law to protect their position.

- Databasing

I know the term “databasing” is vague. I didn’t list it in my previous post, because I didn’t realize that it’s a barrier to entry. But it is in fact quite significant.

The problem is essentially: with our current technology (this might change), is is most efficient to store and access bunch of data with one single, centralized source/system.This is because data is easier to search if you organize it by type. Of course, I’m not talking about physical location, but the system used for organizing data.

For example, Bloomberg is a “Financial Data Vendor,” which, according to Wikipedia, “provides market data to financial firms, traders, and investors.” Bloomberg generates most of their revenue from the Bloomberg Terminal, which you use to access financial data.

This is also how Google makes money: they own a cache of the entire Internet. Can you afford to own such a cache? Only with a lot of money.

- Shared formats

Despite not sounding sexy, this is the main component of “digital coordination.”

Basically, in order for many different devices to talk to each other, they should store information using the same formats.

Suppose all of your company’s data is stored in one format. If you need to pay a licensing fee to the company that maintains the technology behind that format, you’ll do it.

Hence, Oracle got extremely rich by licensing database management systems.

In theory, there is a free market of options, but in practice, there are enormous costs to switching formats because you’ve become dependent on a certain one. To make matters worse, users become acclimated to certain systems (ex: Windows vs Mac).

Branding of luxury goods

The value of branding is predictability: a logo conveys certain information (about standards, what products are available, etc.) People choose a brand they are already familiar with, because it is less effort than sampling everything else.

A luxury good is a superior good in economics, and for our purposes what’s interesting is that they tend to convey status.

By the way, this bleeds into the next category: retail (if this list seems confused, it’s because there’s a lot of overlap).

Land

- Retail

A company like McDonalds makes money from 3 things (1) a business strategy, which they own, (2) a logo and brand, which they own, and which we’ve already gone over, and (3) they usually own the land on which the stores are situated.

In the case of franchises, the franchise company doesn’t even operate the individual stores themselves. They simply collect money (economic rent) off of those that do.

McDonalds is a real estate company! Starbucks is a real estate company! Walmart is a real estate company!

“Retail” is a funny category. You may find it weird that I listed it under land. I could have easily listed it under branding, because branding is also significant. But I believe location is more significant, and location is a function of land.

A franchiser’s business strategy is a replicable method to extract value from a given plot of land. Any incremental value the strategy generates is multiplied across all of their locations. It is a given that land generates rent, so any method which optimizes that rent (franchises!) will be profitable.

- Natural resources

This is pretty straightforward.

- Transport networks

If you are wondering why I include transport networks in “land,” read here.

I would be remiss to mention that economies of scale is a big part of this. The company that uses economies of scale best in the world is Amazon. Hence, Jeff Bezos is the richest man in the world. This is an affect of what I call the “branching problem” here. TLDR: information higher up on the chain can filter down to have exponentially large effects.

Network effects

Read this starting from “Network externalities.” To elaborate, the power of social media companies is that the users generate free content for them.

Regulatory privilege

I’m using this term to refer to the benefit conferred on certain companies via regulations that thwart competition.

With “regulatory capture,” the regulations benefit established firms, usually indirectly or unintentionally. But with Chinese tech companies, the situation is quite more direct.

Alibaba and Tencent could not exist if they were to compete with Silicon Valley directly. They exist because China has laws that hurt or directly ban US tech firms. This allows those Chinese firms to attain regional monopoly status.

Investing

The term “investing” is a bit of an abstraction that obscures exactly how the person made their money, because it’s unclear what exactly they invested in.

When I search “how Warren Buffet made his money” on the Internet, I get many, many articles about advice on investing strategies. Although I’m sure such a thing exists, it’s hard to find what I actually want: a spreadsheet that breaks down in precise detail how much money Buffet made from each investment. It’s obfuscation; people are content to hear generalities over data.

I could try to investigate further. But instead, I’m going to link Peter Thiel’s comments on Buffet, because they’re more insightful than anything I could say. According to Thiel, Buffet has re-tooled his companies as insurance companies in disguise.

Additionally, Thiel claims in another clip that most of Buffet’s investments are exclusive to existing technology, and therefore bets that the industry in that area will not improve. (If you can find this clip, please send it to me).